The World Semiconductor Trade Statistics (WSTS) organization held its bi-annual forecast meeting in Scottsdale, Arizona last month, and one of the topics that seemed to be on everyone’s mind is the impact of tariffs and the trade tensions between the United States and China. The presentation with the most insightful information on this topic was provided by Falan Yinug, Director, Industry Statistics and Economic Policy, at the Semiconductor Industry Association (SIA).

The need to impose tariffs on U.S. imports of semiconductors is perplexing because as of 2017 the United States maintained a semiconductor trade surplus of $2.1 billion with China. In addition, most of the U.S. imports of semiconductors from China are products from U.S. semiconductor companies that are either designed and/or have undergone front-end fabrication outside of China.

In early April 2018, the Materials Research Society held their spring meeting and exhibit at the Phoenix, Arizona convention center. With over 110 symposium presentations, it was difficult to select which sessions to attend. But one forum caught my eye, “AI for Materials Development”. These days AI seems to be everywhere.

As we all speculate about the impact of AI on autonomous driving and the next killer app, Carla Gomes, Professor of Computer Science and director of the Institute for Computational Sustainability at Cornell University, is focusing on large-scale constraint-based reasoning. She pointed out that AI still can’t compete with good ol’ human common sense. Human reasoning and inference planning are still lacking in most AI systems. One of the key fundamentals of AI is building a neural network that resembles the human brain. Even with the advancements of 7nm silicon technology, this is a daunting task, not to mention the complexities of software algorithms to mimic the human thought and decision process.

But in the world of materials development, AI excels. By integrating material experimentation and AI, the discovery of new materials and the application of materials in the real world is progressing at an accelerated pace. AI is capable of developing the hypotheses and—along with robotics—is following through with new scientific discovery.

Major semiconductor foundries have revealed their advanced technology roadmaps for the next few years. They’re all investing billions of dollars into the development of process technologies and packaging options. The number of alternatives has been described as ‘dizzying’. How can all the foundries remain profitable? How does the customer decide which ‘route’ to take?

For the twenty-year period from the mid-1980s through the mid-2000s, process technology nodes were relatively easy to segment. Semico forecasted wafer demand into very clear process technology categories. Starting with the 45/40nm node in 2007, the two major logic manufacturers (Intel and TSMC) along with competing foundries began taking different paths. But the paths were still relatively clear. Intel rolled out their 45nm technology, and then TSMC rolled out their 40nm process. The foundries began to focus on low-power processes first. Then they followed up with their high-performance process several months to a quarter later.

Today, in addition to the number of different nodes, the challenge includes Intel’s claim that their 10nm process is comparable to the 7nm offered by other foundries. Semico believes the matching of product needs with process performance and cost will dictate market acceptance, not the marketing claims of technology-naming convention.

No question, 2017 is expected to be a good year for the semiconductor industry. Semiconductor revenues for 2017 are expected to increase over 9% this year. A 6% increase in unit sales, as well as higher average selling prices for memory products, will help drive the revenue growth rate to its highest level since 2010. Wafer demand is forecast to grow by almost 8%. The higher revenue growth compared to units and wafer demand is a welcome change compared to the last two years. But there are a couple clouds on the horizon.

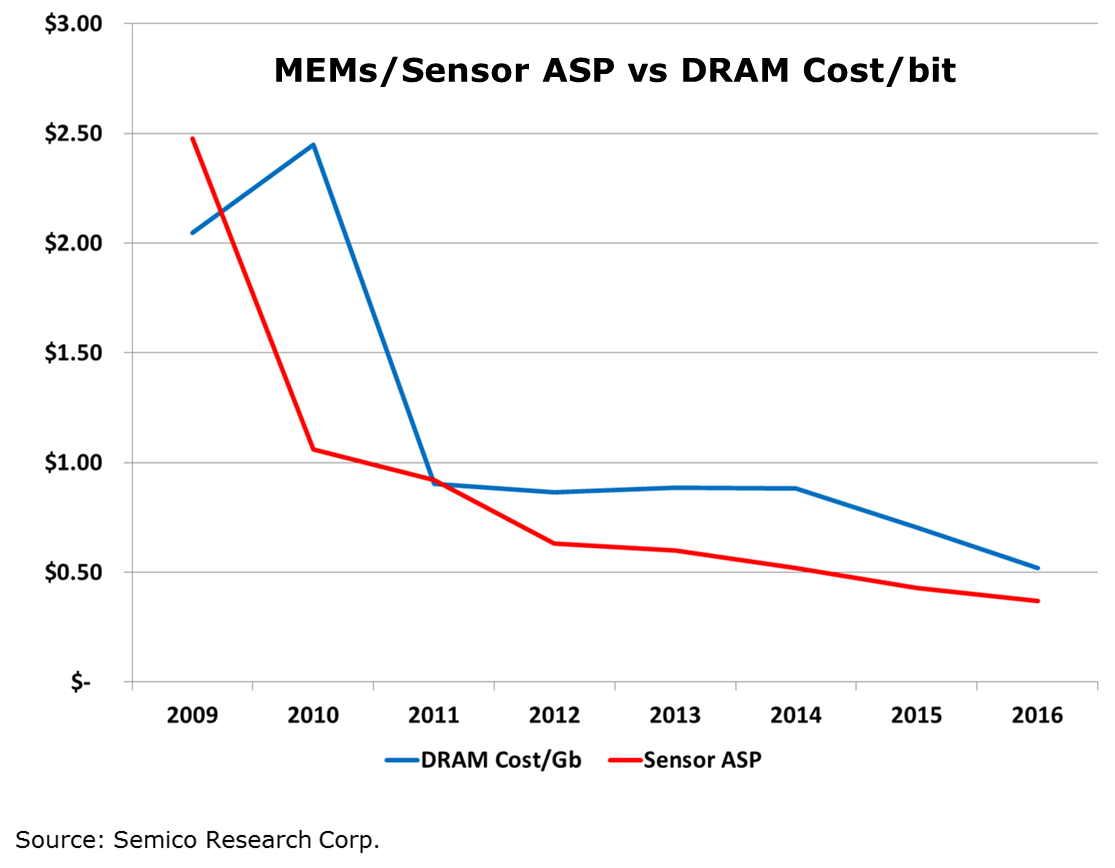

The strong unit growth over the past several years has been at the expense of falling average selling prices. New MEMS and sensor products, the driving forces behind IoT, have experienced steep declines in ASPs. The industry is very familiar with the declines in DRAM cost per bit and how that drives increased applications and demand for memory. Comparing MEMS and sensor ASP declines to that of DRAM, there is a close correlation between the two. In fact, between 2010 and 2016 sensor ASPs fell faster than DRAM cost per bit over the same timeframe.

The MEMS and sensor market continues to be a hotbed for innovation, new opportunities and, as with most new frontiers, there are also some disparate views on market dynamics and strategies. All this was evident at the 2016 MSIG Executive Congress last week in Scottsdale, Arizona.

First, I’ll cover the pioneering and fun subjects. In addition to the Technology Showcase demos and member presentations there were a couple of “outside-the-box” topics such as 3D-printed cars. Co-create was the buzzword on Day 2 and was used by Local Motors General Manager, Philip Rayer, as he showed off several 3D-printed vehicle designs which reduce manufacturing time while integrating a totally digital process and open sourcing options such as an OS battery management system. The company is co-creating an autonomous, electric car with partners such as IBM Watson, Siemens, NXP and Meridian. Rayer challenged the audience to consolidate the MEMS and sensors into a simplified suite of assemblies and reduce the wiring necessary.

Figure: Local Motors Strati 3D-Printed Car

Source: Local Motors

The promise of explosive growth associated with IoT has semiconductor unit forecasts growing at double-digit rates for key product categories. Anything with the word ‘sensors’ seems to be in vogue today. Sensors, image sensors, sensor hubs are all expected to benefit from the billions of connected devices that are forecasted to be in place by 2020. Semico agrees. Unit growth for key products will experience double-digit growth, but with capital expenditures flat to down this year, will the industry be able to support the huge growth?

As the rate of growth for smartphone sales slow, questions arise regarding the impact that slower growth will have throughout the semiconductor supply chain. Over the past decade, the 1 billion-plus smartphone market has driven the need for more advanced manufacturing process technologies, new input materials and the need for more fab capacity. It has even legitimized new players into the supply chain.

Does a slower growth rate mean a change is on the horizon? What portion of the growth is due to semiconductor content versus smartphone unit growth? Semico looked at the change in smartphone silicon content over the past 10 years and the impact on wafer demand.

Although there were smartphones well before the Apple iPhone, it was the iPhone, introduced in 2007, that set the smartphone on the path to the mass adoption that we see today. Between 2005 and 2010, smartphone sales grew at a compound annual growth rate of over 50%. In addition, over that time period, silicon content in a high-end phone doubled. The amount of silicon necessary to produce all the smartphones worldwide has grown from less than 1% of total wafers in 2005 up to over 18% of wafers this year.

The only semiconductor market segment that has not been taken over by the foundries and still remains dominated by IDMs is the memory sector. The memory market is the last bastion for true IDM manufacturers who must be savvy in the changing trends in end market applications, advanced technology development , and must still determine how much and when to invest in additional capacity.

With only four major players, the decision of when to add capacity should be more straightforward; instead, it’s just as challenging as ever. Large memory fabs are inherently more expensive and riskier than ever.

At their Winter Analyst Meeting on February 12th, Micron’s executives touched on a number of trends that memory manufacturers are addressing.

CES is the event that usually gets me energized about the upcoming year; however, this year I almost didn’t attend because I didn’t think there was going to be anything new that would shake up the industry. At the last minute I decided to put on my best walking shoes and fight the crowds. Unfortunately, I think my initial gut feeling was correct.

Sure, there were a lot of people waiting in lines to sit in the new self-driving and electric vehicles or eager to put on the new VR headsets, but there were still several things missing. IoT and power for our mobile electronics need a revolutionary innovation to attain the next level of ubiquitous technology.

First of all, I was disappointed to see so many booths still touting wireless charging solutions aka Powermat. I still have too many charging cables and every month that my phone or Fitbit device ages, the life of the battery charge declines. There were a number of people walking around with a cute, bright green bag that was plugging its ‘Big power, small cells’ product. I wasn’t sure what their product was, but I was definitely curious and feverishly looked for their booth. I was hoping they’d have a product that provided a breakthrough in battery technology or possibly an energy harvesting option. Unfortunately when I got close to their booth, I was handed the cute bag which included a USB charger that was powered by two rechargeable AA batteries. Really?

The vision of the Internet of Things places electronics in all aspects of our lives─from knowing what’s in our refrigerator to life-critical functions such as connected, implantable defibrillators. The potential of autonomous driving places our lives in the hands of sensors, processors and wireless communication that we have to assume collect accurate information, processes that information and reacts in real time. Semico has compiled a list of the top ten elements that must align in order for the IoT to come to fruition. Semico’s report on security started a groundswell of discussion and, more importantly, new solutions from chip vendors.

Semiconductor designers have been engrossed in developing solutions that deliver the right performance at the lowest cost while using the least amount of power. But there is another item to add to the list of essentials for IoT adopton. Making sure your customers know you, or more specifically your product specs, is even more important than ever. In the past five years, packaging has become a critical piece of a successful solution. System in Package, 3D chips, and 3D packaging have all been created to serve one or more angles of the power/performance/cost pyramid. What about the results once the chip is mounted onto a board with all its companion chips? How far should the chip manufacturer go in order to control and guarantee performance and reliability in their chips?